A few practical examples of the use of blockchain in our daily lives

Blockchain is one of the biggest buzzwords right now. Blockchain is an advanced technology that already has vast implications, transforming not only financial services, but also other fields of business.

A blockchain is a distributed database, which means that the database's storage peripherals are not all connected to a common processor. The blockchain keeps a growing list of organised records called blocks. Every block has a timestamp and a link to a previous block.

The cryptography guarantees that users can modify only the parts of the blockchain in their possession if they have the private keys needed to write the file. It also guarantees that copies of the blockchain distributed to all members are synchronised. This technology is growing fast as demonstrated by blockchain developers' latest recruitment figures.

Blockchain has a promising future and many examples of solutions are springing up in the United State, including in mass retail, finance, insurance, and energy distribution.

Blockchain and energy

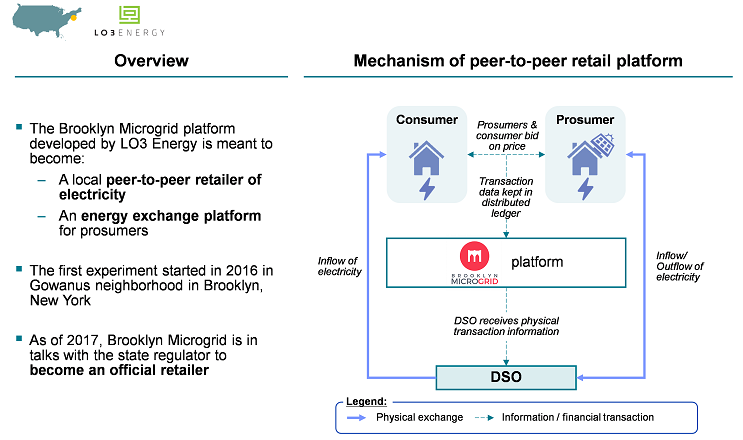

In Park Slope, a district of Brooklyn, neighbours buy and sell solar energy to and from each other on a blockchain platform. This allows them to make payments and maintain the system and level of energy in case of disaster. The various storms that have hit the city over the last decade pushed certain inhabitants to install solar panels, meaning they no longer need to rely on energy suppliers.

Some of these users cannot consume all the energy generated by their solar panels, so they resell part of their electricity. In April 2016, the first transactions were made between neighbours who didn't have their own solar system and others with excess solar electricity. With the help of the start-up LO3 Energy, the inhabitants of Park Slope and the neighbouring districts of Gowanus and Boerum Hill set up the Brooklyn Microgrid.

These kind of peer-to-peer business transactions - made directly from computer to computer - are very profitable and have great potential. Blockchain technology enables identification and confirmation of each transaction and, as a result, helps to transform this district into an electricity supplier.

Blockchain and housing

Brooklyn clearly takes blockchain experimentation seriously. Another district, Bushwick, is the setting for a new blockchain technology innovation on the New York housing market.

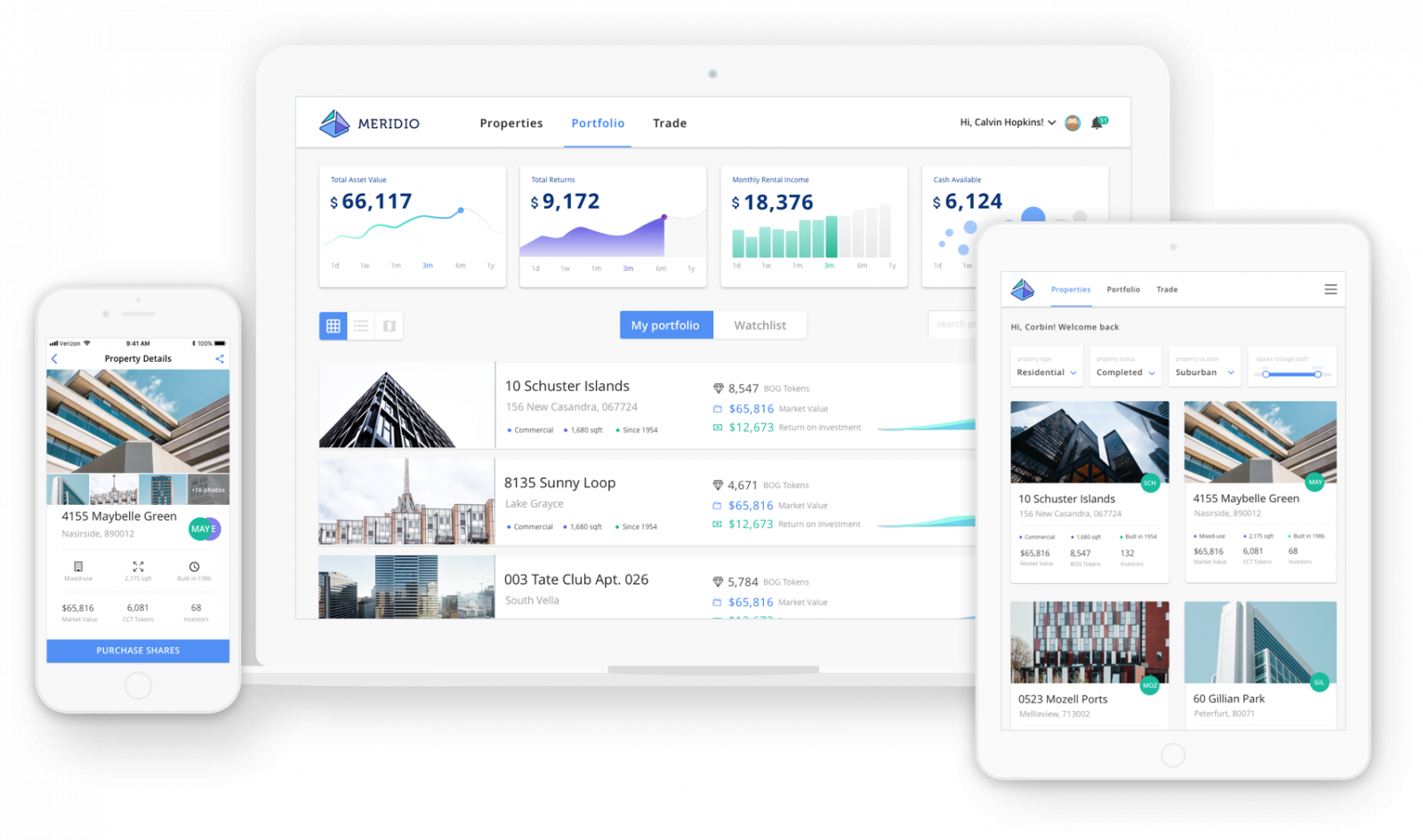

Meridio, a start-up supported by ConsenSys Media (a very well-known blockchain information site in the United States), improves the way investors manage their real-estate investments. Meridio's experiment involves introducing a crypto-currency token for the eight current investors who own the test property at 304, Troutman Street in Brooklyn. Using the underlying blockchain platform, an encrypted digital record of quasi-instantaneous peer-to-peer transfers, investors will be able to sell, buy and document all aspects of their investment using the token.

Business between existing investors looking to buy or sell becomes faster, but the token also makes it possible to reduce entry barriers for investors with no significant capital to invest.

If you don't have the money to buy your house or apartment, you can buy a bit of one using these tokens because one of blockchain's advantages is that it allows real-estate assets to be divided. Transaction fees will be much, much lower due to the use of peer-to-peer technology.

Meridio isn't the first company to suggest using crypto-currency and blockchain to transform real-estate management in New York. Last March, a group of investors launched the idea of making an initial offering of crypto-currency for a token that would then be used to purchase a majority shareholding in the Plaza Hotel.

The real-estate market is making progress and blockchain could be a major asset to boost it and attract small investors.

Blockchain and e-commerce

Blockchain appears to be THE technology to give consumers back power over their data. In e-commerce, blockchain can decentralise a consumer database. So instead of being faced with a company that knows all a consumer's clothing preferences, this information is distributed along the blockchain, with the consumer holding this information. This is the how it is used by a firm like Every.

Every's concept uses a blockchain-based e-commerce system offering consumers even more power by giving them control over their data and letting them choose the brands that can use it.

In this case, the blockchain decentralises and creates an anonymous user database in which buyers and brands can see different data points. But with Every, consumers decide how much of their data they want to include in the blockchain (gender, size, clothing preferences, etc.). These consumers can then decide which brands can access this data in return for rewards such as discounts or loyalty benefits.

Every's aim is to get away from the centralised retail trade format as it exists today, with buyer information and data organised by a "handful of technology firms", particularly Amazon. According to Every's executives, Amazon's user data allows the company to determine which products will be offered to users and to use this information to create own brands that prevent other brands from succeeding on the market.

By creating an Every account, consumers have a shop digital wallet. This means they can reveal and store some personal information as well as data on their buying habits, then exchange this information for tokens that serve as rewards and discounts and in certain cases can be used to make purchases.

The business plans to put 1 billion of its tokens up for sale from 14 May 2018.

450 million tokens will be distributed to brands that can use them as rewards for online buyers. As explained earlier, these customers can decide on the quantity of information they want to disclose to the brand, wrestling back control over their information.