H1 2018 Results Improvement in operating indicators and confirmation of full-year objectives

In the first half of 2018, SQLI’s recurring operating income rose 15% on the back of 13% growth in turnover, while the Group’s key indicators (employment rate, operational excellence and contributions from international projects) all improved.As a result, SQLI confirms its 2018 objectives and its 2020 roadmap.

Turnover up 13%

Growth was driven by development services for digital platforms in France and throughout the international network, which now represents 63% of business (versus 52% in first-half 2017). These core services were mainly performed for major companies, and the move upmarket resulted in the average daily billing rate rising 4% to €586.

Fueling this move upmarket is the SQLI Group’s recognized position as Europe’s benchmark digital experience firm (source: Forrester) and a digital commerce expert, gained in large part thanks to its expertise in industry-standard technological platforms (SAP Hybris, Magento, Salesforce, Oracle Commerce Cloud, etc.), which are essential for maintaining key accounts’ digital leadership.

Outside France, Group turnover climbed 57% to €40.4 million, driven by strong organic growth of 6% and the successful integration of Star Republic (acquired in May 2017) and Osudio (acquired in September 2017). As a result, the international network represented 35% of billing in the first half of 2018, versus 26% in the same period in 2017.The growing synergies between the business activities of the international subsidiaries, the technological expertise of the Group’s various entities and the digital services centers (near- and offshore) took tangible shape in the first half of the year, particularly through the implementation of platforms for Jotul, ArcelorMittal and Fressnapf.

In France, the Group recorded organic growth of 7% outside of Paris and an 11% contraction in the capital, reflecting fierce competition for talent and the ongoing transformation of the organization. The first signs of improvement were visible at the end of the six months, with a sharp decline in staff turnover and continued increases in the employment rate.As a result, consolidated turnover amounted to €115.9 million in the first half, up 13% on the prior-year period (up 1% at constant scope and exchange rates).

Significant improvement in Ebitda and recurring operating income

The Group’s key indicators all improved during the first six months of the year, buoyed by turnover growth, ongoing productivity gains and the cost reduction strategy introduced in 2017 and continued in 2018. Staff turnover, for example, declined to 22%, which is broadly in line with industry standards. The employment rate rose from 83.1% in the first quarter to 85.0% in the second quarter. Structural costs were reduced by 3 points in one year, coming in at 20% of turnover.

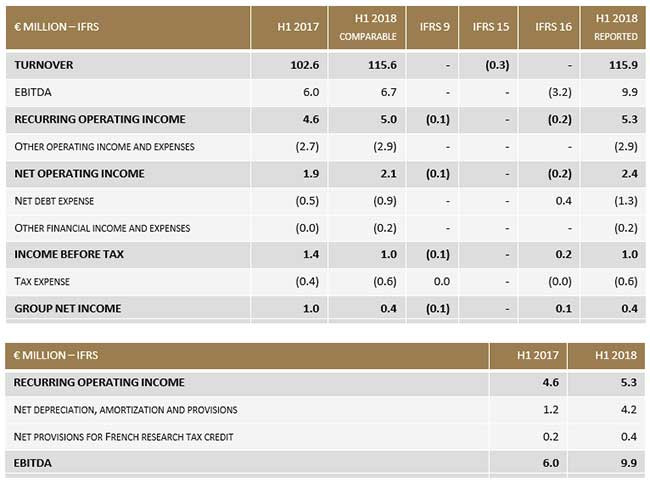

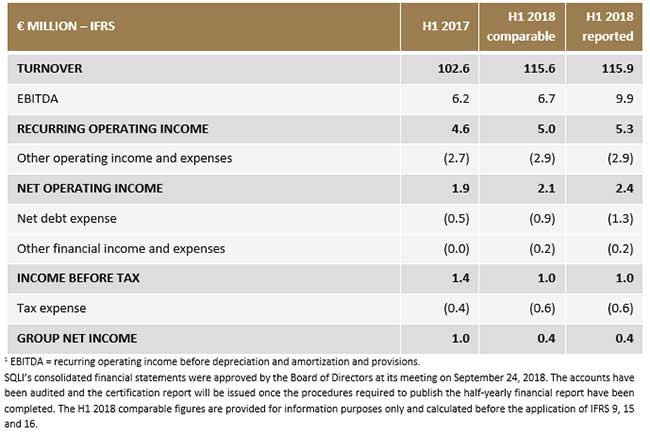

Recurring operating income thus climbed 15% to €5.3 million, or 4.6% of turnover. The operational excellence of the subsidiaries proves the significant potential for the Group to improve its profitability, with recurring operating margin exceeding 14% of turnover in Switzerland and 9% in Northern Europe.EBITDA amounted to €9.9 million, reflecting the first-time application of IFRS 9, 15 and 16.

Other operating expenses came in at €2.9 million, including costs relating to restructuring (€1.0 million) and relocation (€0.9 million), lifting net operating income 25% to €2.4 million. The Group confirms its ambition of significantly reducing its annual non-recurring expenses (€6.4 million in 2017).

Net of its debt expense of €1.3 million and a tax expense of €0.6 million, SQLI posted net income of €0.4 million for the period.

Solid financial position

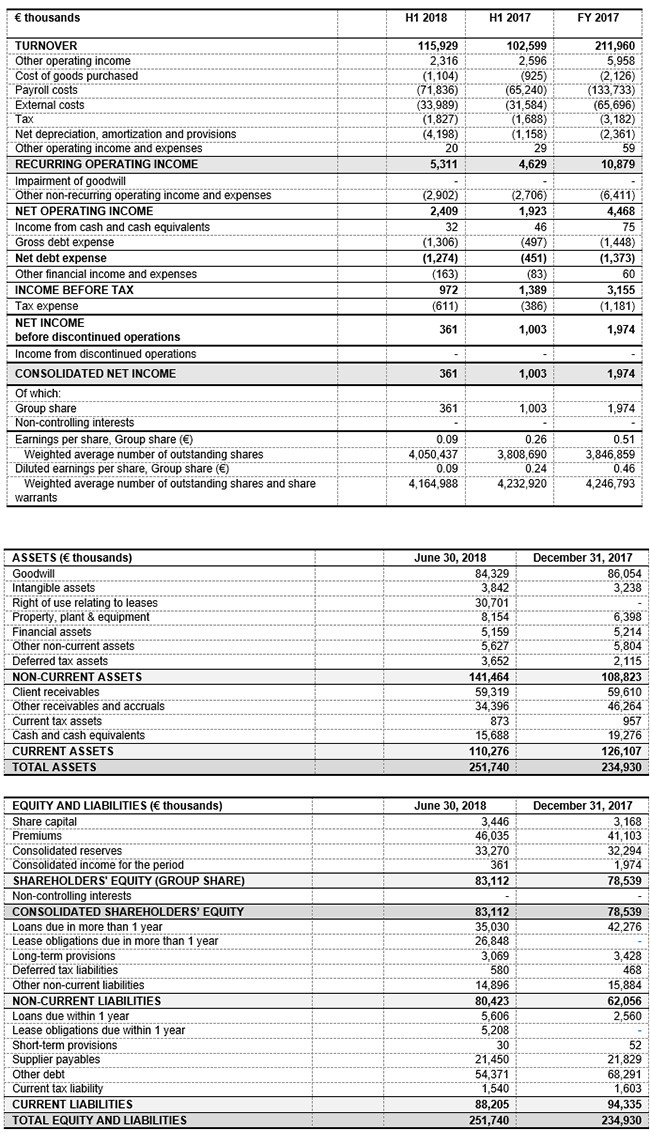

The careful management of cash flow from operating activities (a positive €0.4 million at June 30, 2018 versus a negative €5.6 million at end-June 2017) and the €5.2 million in income from the issue of share warrants (BSAARs) enabled the Group to finance investments while continuing to repay its bank loans. At June 30, the Group’s net debt came to €24.9 million, an improvement on the €25.6 million at December 31, 2017, with shareholders’ equity of €83.1 million.

Objectives confirmed

Bolstered by the dynamic market and the internal measures implemented, SQLI anticipates that it will achieve the full-year objectives announced in July: turnover of €240 million, reflecting a combination of double-digit year-on-year growth (from €212 million in 2017) and the completion of a targeted acquisition, and EBITDA of more than €23 million.

This will put the Group on the path to achieving the goals of the Move Up 2020 plan, which forecasts double-digit average annual growth and EBITDA in excess of 14% (taking into account the impact of applying IFRS 9, 15 and 16, which is estimated at around 2% in the long term) by the end of the plan.SQLI will publish its third-quarter 2018 turnover on November 8, 2018 after the close of trading.